A detailed business research note is already available as part of the microcap stocks series

Interarch Building Products Ltd is one of the limited capex linked stories that can offer 25%+ ROCE across market cycles at minimal balance sheet risk. As of September 2024, the balance sheet had a balance sheet size of ~1,100 Cr with the net fixed assets base at just 215 Cr and cash equivalents of ~400 Cr. It is one of the very few businesses that can offer high asset turns (>6x) at low working capital intensity (< 40 days) and healthy operating margins of 9-10%.

It is the second largest player in the Pre-Engineered Buildings (PEB) segment in a consolidated industry structure where ~80% of the organized market is controlled by the top 5 players. With Corporate India being in the best balance sheet shape it has been for many years, further expansion by the largest corporates in India can translate into healthy demand and double-digit growth rate for the business.

All of these points are known by most market participants as well. Hence, we will focus on why we like the business now and what numbers the business can print over the next few years.

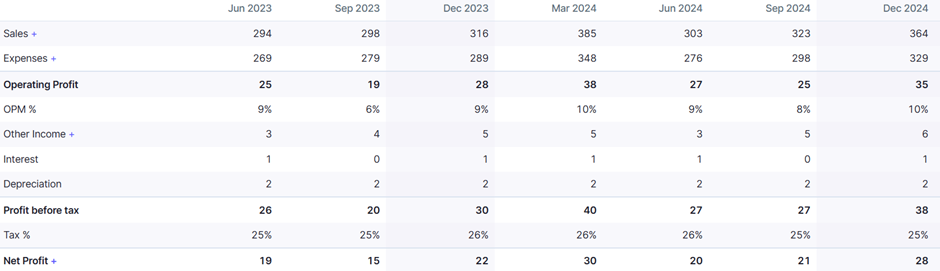

Recent Financials

The business has been delivering a good set of numbers over the past 5 quarters. While the revenue growth appears muted due to steel price volatility, the underlying volume growth has been in the range of early double digits through the period.

A cursory glance at the financials of the market leader Kirby Building Systems indicates that 10-11% is the operating margin for a well-run business that is running at optimum utilization. Kirby operates at negative working capital and has ~400 Cr cash on books. Interarch has hit 10% operating margin for Q3 FY25 and is likely to print a similar number for Q4 FY25 too.

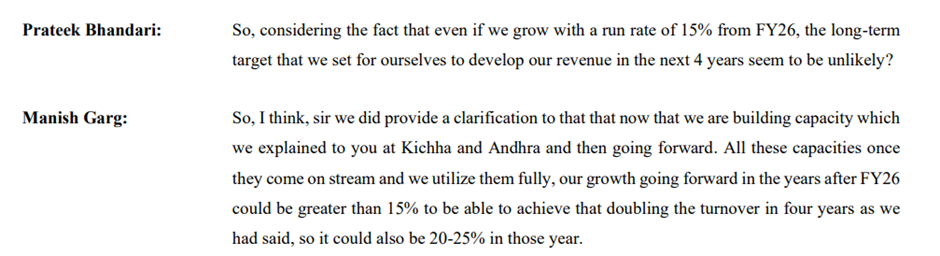

Capex plans, order book & growth guidance

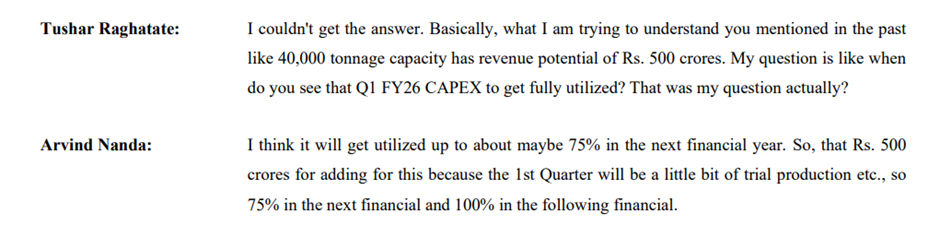

The ongoing capex that is expected to get commissioned by Q1 FY26 should add 40,000 MT to the existing capacity of 160,000 MT, this incremental 40,000 MT offers a revenue potential of 500 Cr which is expected to contribute to revenue starting from Q2 FY26. Phase I of the capex was commissioned in Sep 2024 at an investment of 40 Cr. Another phase of capacity for 85-90 Cr will be starting in Q3 FY26 for expansion at Gujarat.

The management has reiterated revenue growth guidance of 10% for FY25 and 10-15% for FY26. The PEB industry is expected to grow at 9-10% p.a. over the period FY24-FY29.

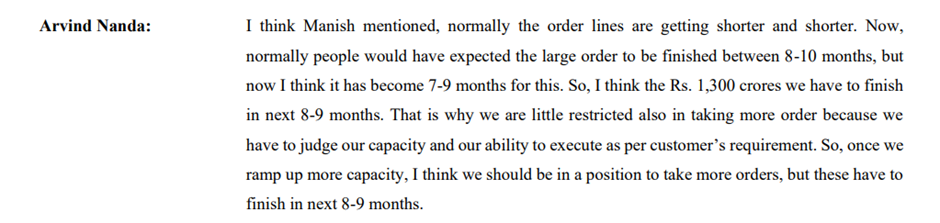

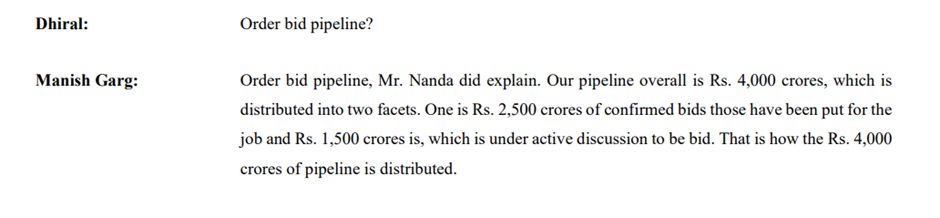

Total order as of Dec 31, 2024 stands at 1,305 Cr, order inflow during Q3 FY25 was ~405 Cr. Execution of the order book takes between 8-10 months going by the historical execution rate.

Important Snippets from the Q3 FY25 earnings call

In our assessment, this is one of the very few businesses where aggressive capacity addition is unlikely to dent the balance sheet or the P&L even if the anticipated demand does not come through. With ~400 Cr on the balance sheet and an operating ROCE > 25%, funding capex should not be a challenge at all.

If the corporate capex theme does turn for the better from FY26, Interarch will be a clear beneficiary since it is an early-stage capex play (the services and products of the business are needed at the project initiation stage and not closer to the completion of the project).

Risks to Note

- One of the risks that can play out is P&L volatility due to steep fluctuation in steep prices. With the global environment seeing a lot of policy action, this scenario cannot be ruled out

- The risk of earnings stagnation at short to no notice is possible in the case of most capex plays. In the case of Interarch, this risk is present but to a much lesser extent compared to other Govt and PSU driven capex plays. If private capex stays at the current level and doesn’t translate into higher order book for the business, it is possible that one could have 1-2 years of flat earnings growth since operating leverage has already played out through FY25

- There is the risk of the market clubbing this business with much higher beta names in the Infra, EPC & Construction space which may keep a lid of valuation multiple. We believe that this business can trade at higher multiples compared to the other business models but the market may paint all capex stories with the same brush if core sector activity does not pick up through FY26

Projections & Valuation

Our assessment is that balance sheet risk is minimal in this business. The risks one would need to hedge for are valuation risk and the risk of earnings growth coming in lower than expected.

The P&L structure is very simple, hence does not call for a detailed modelling exercise.

FY25 PAT is likely to be in the range of 100-105 Cr. The business is trading at 24-25x FY25E PAT.

If the planned Andhra Phase II capex commissions on time and the utilization turns out to be 75% as per management guidance, revenue growth for FY26 could be higher than 15%. Earnings growth for FY26 is largely expected to be in line with revenue growth, FY26E PAT could be in the range of 120-125 Cr. The business currently trades at 20-21x FY26E PAT.

Ideally one should buy this business closer to 20-22 TTM PE but the current valuation is in the fair zone. Our preference would be to take an initial position and add the rest over the next 1-2 quarters.

Technical View

We do not have a long enough history to offer a nuanced view.

Both in a fundamental and technical sense, the range of 1300-1350 could offer a good entry point if the opportunity presents itself in the ongoing correction.

Disclaimer

Every single disclaimer you have ever read in the investment world would apply here. This report summarizes our views on the specific business based on the information available to us at the time of writing the report. We have taken due care to ensure the correctness of the data in this report, however we too are human and may have made some inadvertent mistakes. The report has certain projections and forward-looking statements that may not turn out to be as accurate as we intend them to be. Investing is a probabilistic gamble for the most part, there is a very high probability that some or even many of the projections here will turn out to be wrong.

This business is just one of the many bets that we may end up taking as part of the equity advisory service we offer. Our unit of measurement is the overall portfolio performance and not the individual business under question. Please do not take a position based solely on this report unless you are already a customer for whom we have done a proper risk profiling exercise and we have mutually signed a document that details the terms and conditions of the advisory service. Our approach is to manage risk at the portfolio level through allocation to various sectors, business models and we invest across styles and market capitalizations. We practice adequate diversification and so should you.

All IP rights for this report rest with us. Please feel free to learn from this report if you find this worthwhile but please do not reproduce or circulate this report without prior permission. You will be violating confidentiality norms if you do so, this report is only for subscribers to our equity advisory service. This report is not an attempt to solicit business, neither in India nor in any other country.

We wish you good luck in your investing endeavors, we investors are going to need it!